- April 7, 2025

-

-

Loading

As consumer demand centers around a digital approach to banking, the traditional way of community banking — locally-based institutions where customers know their teller and the bank president is a civic leader — is slowly disappearing. In response, the handful of community banks that remain in the region are shifting strategies in order to stay relevant.

The decline of community banks nationally is significant. A study released in 2020 by the Federal Deposit Insurance Corp., for example, showed a 30% drop in community banks in the U.S. between 2012 and 2019, from 6,802 to 4,750. The primary cause? Voluntary mergers.

On a local basis, in the late 1990s, a high-point for community banks in the Sunshine State, there were more than 40 community banks based on the west coast of Florida. Now there are less than 15. On an even more hyper-local basis, in the past 15 years, the number of Lee County-based community banks has fallen from 12 to 2, while in Collier the tally has dropped from nine to one.

With more and more community banks exiting the market, in acquisitions and mergers, it leads to both a philosophical and tangible question: what is the future of the community bank?

“Unfortunately community banks in Florida and the nation are going in the opposite direction,” says Kyle DeCicco, president of Sanibel Captiva Community Bank, adding the trend may be around for good. “It’s hard to compete. We’ll continue to see that.”

One of the more recent trends in community bank mergers is credit unions buying community banks. That's particularly interesting because as Corey Neil, Bank of Tampa CEO, explains, the clientele within each institution is wildly different.

“I suspect the challenge for credit unions will be to figure out how to serve a market they have not traditionally served,” he says. “I’m interested to see how being able to merge those two markets will work in a credit union/bank acquisition strategy.”

A key driver in this trend is credit unions seeking to achieve economies of scale, in addition to new geographic locations. Aside from building new locations, an acquisition of another financial institution is a quick way to scale up a credit union.

With all that going on, how do community banks continue to survive while also competing against large brands? The answer is two-fold. And DeCicco says it starts with loosening regulations.

“Regulation is a big part,” he says. “If we want more community banks, we have to deregulate a bit. We have to make it more difficult for a credit union to acquire a bank.”

If nothing else, the deregulation, including less capital requirements, might end up helping new community banks pop up.

Between 2000 and 2010, there were 1,292 new bank charters reported by the FDIC. There were only 49 reported through 2021. “It would allow ease for new banks to be chartered,” he says.

DeCicco also acknowledges the community bank's future boils down to each individual institution. Some banks scale up in hopes of being acquired while others choose to stay relatively small.

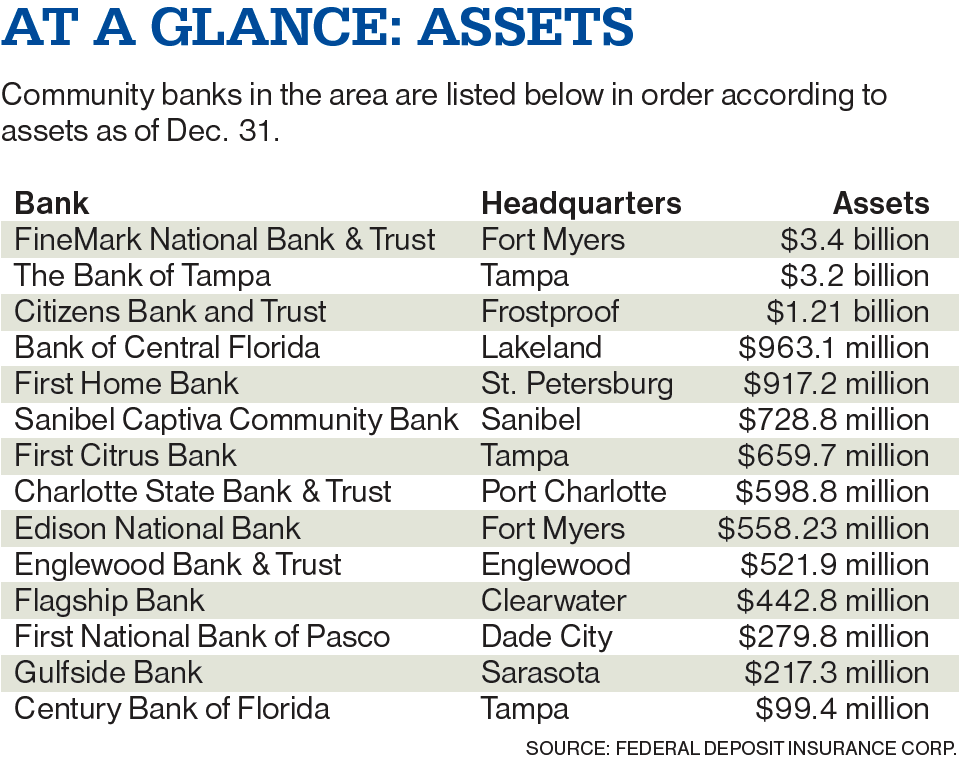

Sanibel-based Sanibel Captiva, with $728.8 million in assets through Dec. 31, is focused on the latter, he says, which includes not expanding outside of Southwest Florida. DeCicco says the strategy is to take in local deposits and lend out to the community. “The board plans to keep it that way,” he says. “We’re looking for small, conservative growth but that’s not the goal.”

Instead, the community bank has a goal of returning a fair dividend to shareholders as well as taking care of its 110 employees and the community. “As long as we do that,” he says, “we’ll be OK.”

Even though community banks are smaller in nature, the sector has some heft to brag about: in 2019, the FDIC reported community banks held 36% of the industry’s small business loans and 70% of agricultural loans. That would be difficult for a big bank to jump into.

Neil McCurry president and CEO of Sarasota-based Sabal Palm Bank, offers a solution for community banks looking to both survive and thrive, beyond the stay small or get acquired approach DeCicco mentions. McCurry's advice? Put a bear hug on going digital.

“The bank industry is continuing to evolve because of technology,” he says. That goes for features like mobile banking, automated loan underwriting, online loan applications, remote deposit capture, interactive teller machines and electronic bill payment. “Banks thrive with advances in technology."

McCurry, who has been in the industry for over three decades, founded People's Community Bank in Sarasota in 1999 and joined Sabal Palm in late 2012 as CEO. He followed his own advice at Sabal Palm, investing in the bank's technology for several years. That partially led to Sabal Palm itself becoming an acquisition target. Stuart-based Seacoast Banking Corp. of Florida, in a $53.9 million deal announced last August that closed in January, is the new owner of Sabal Palm, which is keeping its brand in the local market as a division of Seacoast National Bank. The Sabal Palm sale leaves Sarasota-based Gulfside Bank, founded in 2018, as the only locally-based community bank in the Sarasota-Bradenton market.

"Any institution that thinks it can survive on tech alone will have a challenge." — Neil McCurry, Sabal Palm Bank

Maintaining relevance, then, in one big sense, lies in relying less on cash currency and more on digital payments.

“I think the smaller banks will do well with a proper marriage between technology and personalized services,” McCurry says. “Any institution that thinks it can survive on tech alone will have a challenge.”

Not only is it tough for community banks to survive, it's tough to get going. “Capital requirements to start a new institute is getting harder and harder,” DeCicco says.

Take Sanibel Captiva for example. The bank got started with $6.5 million in capital. That was in 2003 and DeCicco says Craig Albert, CEO and founder, was able to raise that quickly. “Now, it’s quadruple that,” DeCicco says, noting it would take upward of $20 million in capital to start a small bank.

Some startup community banks have been able to overcome that threshold. In 2017, for example, Gulfside Bank President and CEO Dennis Murphy raised $23.5 million over eight weeks when he founded his Sarasota bank. Longtime banker Bill Blevins, meanwhile, sought to raise between $20 and $25 million when he was in launch mode for Fort Myers-based Gulf Coast Business Bank last year. By April, he announced on the bank's website he raised $23.6 million. And Clearwater-based Waterfall Bank raised $45 million before it opened last October.

Yet another challenge community banks face? Adapting to a new business model. McCurry, with his years of experience, says he would essentially forget everything he’s learned up to this point. Instead, the focus would be on incorporating remote working and technology into the new community bank.

That’s something Neil, with Bank of Tampa, agrees with. “There would be a commitment to digital right out of the gate, which probably means more investment in technology and less investment in physical offices,” he says.

But Neil also errs on the side of caution with investing in the digital model.

“Because community banking is all about relationship building, (you) would have to make that technology investment without ignoring the importance of one-on-one engagement,” he says. “You have to figure out how to do both.”

During the pandemic, the community bank model was validated with a shining star moment. When the Paycheck Protection Program was launched in spring 2020, with billions of dollars in forgivable federal government loans, community banks rose to the occasion. Overall, community banks handled 60% of all PPP loans, according to the Independent Community Bankers of America organization. On a local basis, banks like Sanibel Captiva and Sabal Palm set up war-room like centers, with bankers working nights and weekends — that included Easter Sunday at one bank— to get through the deluge of PPP applications. This came as the country's banking behemoths, like Wells Fargo and Bank of America, struggled to shift quickly to meet the demand.

“I think that gave us a nice shot of confidence in the role of a community bank,” Neil says.

Promoted to CEO of the Bank of Tampa, with $3.2 billion in assets, in January, Neil says in order for community banks to flourish, they’ll need to invest in a variety of ways to engage with clients to provide the best experience — whether it’s mobile banking, in-person or through the smartphone.

“The super regional or national banks have the scale that they can make those investments,” he says. “Our bank has achieved size and scale enough that we can make those investments and that is very much our strategy going forward.”

Hurtling toward a more digital approach is not anything new in banking, per se. It's just happening at rapid-fire pace. “I think it’s been happening for the last 10-15 years,” Neil says. “The basic concepts of transacting business digitally has already been in place. What has changed, and I think is causing the acceleration, is the clients weren’t forced to deal with banks that way.”

Before the pandemic, customers had an option of how they wanted to bank. But the last two years temporarily eliminated traditional, in-person banking. As a result, the industry was forced to adopt mobile banking at an accelerated pace. And that’s something that isn’t going to change tomorrow.

Neil says the Bank of Tampa intends to roll with all these changes, and while he knows the bank "cannot be asleep at the wheel,” as the industry drives into the future, he also doesn't want to lose the part of the bank that drew customers there in the first place.

“We acknowledge clients want to bank and transact business in ways that are most convenient to them,” he says. “So we will continue to build out our digital channel to provide that convenience while we still preserve what makes us special, which is the ability to pick up the phone and have another person on the other line.”